· Greenback· Importance of Understanding Cash Flow

The Cash Flow Mistake Most People Don't Know They're Making

Most people think they have a spending problem. In reality, they have a timing problem. Here's a scenario that might sound familiar: you earn a solid income, you're not living extravagantly, and yet somehow you're still running low before the next paycheck hits. You're not broke — you're cash flow blind. And it's one of the most common financial mistakes that rarely gets talked about. Cash flow isn't just a term for businesses. It's the rhythm of money moving in and out of your personal accounts, and when you don't understand that rhythm, even a healthy income can feel like it's never enough.

What Is Personal Cash Flow (And Why Most People Ignore It)

Personal cash flow is simply the relationship between when money comes in and when it goes out. Your income arrives on specific dates. Your bills, subscriptions, loan payments, and everyday spending hit at different times throughout the month. The gap between these two patterns is your cash flow — and most people have never actually mapped it out.

Instead, they rely on a single number: their checking account balance. If the balance looks okay, everything feels fine. If it's low, panic sets in. This reactive approach is the core of the problem. A checking account balance is a snapshot; cash flow is the full movie. And without seeing the full movie, you're making financial decisions based on incomplete information.

The Mistake: Budgeting Without Timing

The classic budgeting approach goes something like this: add up your monthly income, subtract your monthly expenses, and whatever's left is what you have to work with. On paper, the math checks out. But in practice, it falls apart, because a monthly budget treats all 30 days as equal, and they're not.

Consider this: your rent and car payment both hit on the first of the month, your insurance auto-debits on the 10th, and your paycheck doesn't arrive until the 15th. For the first two weeks of every month, your account is under pressure — not because you overspent, but because your expenses are front-loaded and your income is back-loaded. That's a cash flow mismatch, and no amount of budgeting discipline will fix it if you're not aware it exists.

This is the mistake most people don't know they're making. They blame themselves for poor spending habits when the real issue is that they've never looked at the timing of their money.

What Cash Flow Blindness Actually Costs You

When you can't see your cash flow patterns, the consequences go beyond the stress of a low balance mid-month. You start relying on credit cards to bridge gaps that wouldn't exist with better timing. You miss opportunities to move money into savings or investments because you're never sure if you can afford to. You pay overdraft fees or dip into emergency funds for what are actually predictable shortfalls. Over time, these small costs compound. A cash flow mismatch of just a few hundred dollars at the wrong time can trigger a chain reaction of late fees, interest charges, and missed savings contributions that adds up to thousands over the course of a year.

How to Fix It: See Your Cash Flow Clearly

The good news is that solving a cash flow problem is far simpler than solving a spending problem — once you can actually see it.

Track income and expenses by timing, not just totals. Knowing that you spend $3,000 a month is useful. Knowing that $2,000 of that hits in the first ten days is transformative. When you can see daily, weekly, and monthly spending breakdowns alongside your income schedule, the mismatches become obvious.

Align your bills with your income. Many billers allow you to change your payment date. If your paycheck lands on the 1st and the 15th, redistribute your bills to land shortly after each payday. This single adjustment can eliminate the cash flow crunch entirely.

Build a small cash flow buffer. This isn't the same as an emergency fund. A cash flow buffer is a small cushion, even $500 to $1,000, that sits in your checking account specifically to absorb timing gaps. It prevents you from dipping into savings or relying on credit for predictable shortfalls.

Review your cash flow trends regularly. A single month won't reveal much, but when you track your income versus expenses over weeks and months, you'll start to see recurring patterns. Those patterns are the key to planning ahead rather than reacting after the fact.

Stop Blaming the Budget. Start Reading the Flow

If you've ever felt like your budget should be working but somehow isn't, there's a good chance the issue isn't what you're spending, it's when. Cash flow visibility turns a frustrating guessing game into a clear, manageable system.

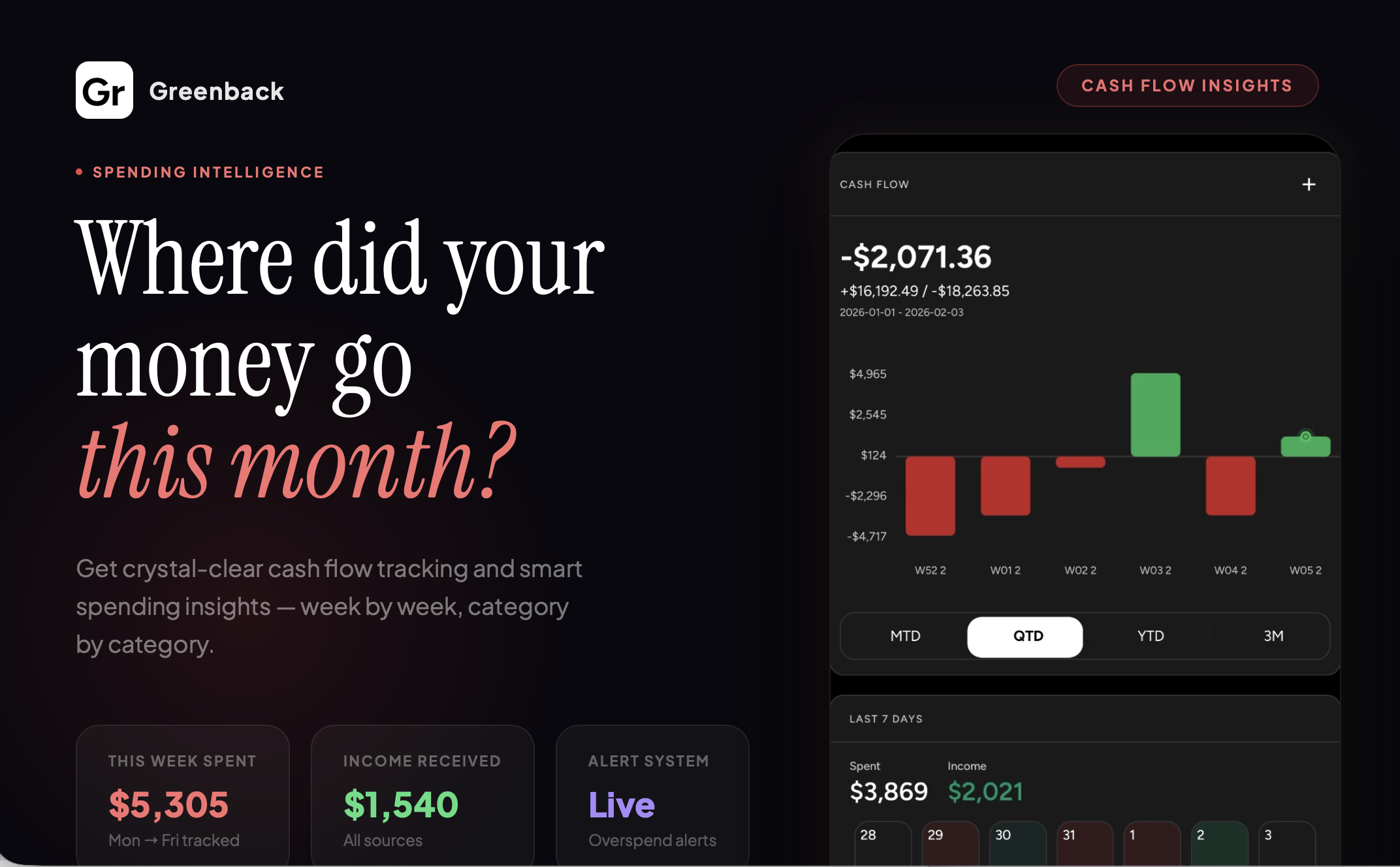

Greenback makes this easy by showing your income versus expenses at a glance, with daily, weekly, and monthly breakdowns that reveal exactly how your money moves. When you can see the flow, you can finally control it.

Your budget tells you where your money should go. Your cash flow tells you where it actually goes, and when. Pay attention to both.